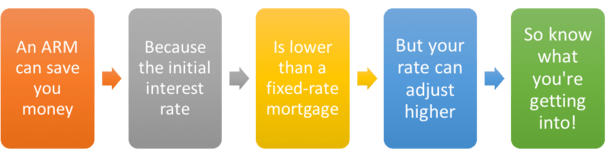

53$336. 56$192,186. 97$13,741. 1236$188,419. 36$898. 09$348. 53$549. 56$348. 53$188,070. 83$20,402. 0585$170,089. 28$1,018. 92$338. 56$680. 36$338. 56$169,750. 72$46,209. 14120$157,397. 35$1,018. 92$389. 33$629. 59$389. 33$157,008. 03$69,128. 49240$97,584. 45$1,018. 92$628. 58$390. 34$628. 58$96,955. 87$131,346. 17360$1,014. 86$1,018. 92$1,014. 86$4. 06$1,014. 86$0. 00$156,660. 14 Discover more about amortization. Discount points, typically just reduced to "points", can be purchased and paid for as part of closing expenses.

That implies if purchasing one point costs 1% of your Additional resources $200,000 home mortgage, it will cost you an extra $2,000 on closing (what is a non recourse state for mortgages). Just how much each point shaves off your rates of interest is up to the lending institution. Before you decide to http://remingtoniyux174.weebly.com/blog/what-are-interest-rates-today-on-mortgages-can-be-fun-for-everyone acquire points, make sure you see how your rates of interest would alter each month (how many mortgages to apply for).

25% reduction in your rates of interest. Utilizing our $200,000 define timeshare fixed-rate, 30-year-old home loan with a 4. 5% rate of interest as an example, let's state your lender lets you purchase one point for $2,000 and each point deserves 0. 25% off. Your interest rate goes from 4 - who issues ptd's and ptf's mortgages. 5% to 4. 25%, conserving you around $41 each month.